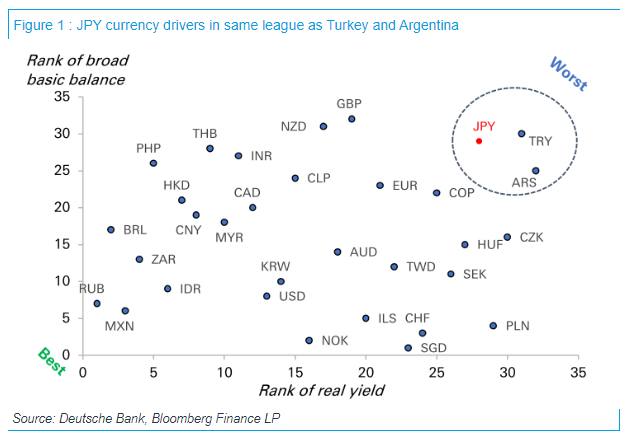

Japanese intervention to defend the yen will at best be ineffective and at worst make the situation worse. Why? Because a simple glance of the yen’s drivers - yields and external accounts - puts the Japanese yen in the same league as the Turkish lira and Argentian peso. Not only does Japan have the lowest nominal yield in the world (and the only economy with negative rates), but also record low real yields, a direct function of the BoJ’s refusal to tighten policy in the face of high inflation. Japan now also has one of the worst broad basic balances in the world – not on the back of a large current account deficit but because the BoJ has effectively engineered slow-motion capital flight from domestic investors into foreign assets. If you are Japanese, what is the point of buying a 5-year JGB with a nominal yield of 50bps when you can buy a 5-year US treasury with a real yield of 3%?

The “solution” to therefore stabilize the yen is simple: the Bank of Japan needs to stop QE and start hiking rates. On the flipside, FX intervention is likely to achieve the opposite: by selling dollar reserves (treasuries) it will likely put further upward pressure on US yields and support the dollar. More critically it will lead to a deterioration of the Japanese government’s external balance sheet and by extension its fiscal position. This, together with the fresh fiscal spending that is being announced is the opposite of what should be happening in an environment where the cost of government funding is starting to rise.

The UK crisis last year showed how markets can react abruptly to policy that is perceived to be off-kilter. In Japan’s case however, these non-linearities are unlikely to show up in the bond market. The BoJ owns the near-entirety of the stock of ten-year bonds and more than half of all JGBs. The price formation mechanism in fixed income is effectively suspended, inclusive of 5y5y inflation breakevens at less than 1%. Instead, the transmission mechanism of market pressure will have to happen solely via the exchange rate. The way this works is simple: accelerating capital outflow as real yields keep moving deeper into negative territory.

Krugman famously wrote that for Japan to move out of deflation, the central bank has to follow irresponsible policy: stay dovish even as inflation is rising. The central bank is most certainly living up to this promise. But as the policy setting becomes more and more extreme, the risks around non-linear moves in the market go up. At the moment, yen volatility remains very well contained and option market risk reversals suggest the next big move in USD/JPY will be down, not up. This is telling us that the market still believes that the BoJ will ultimately do the “right thing”: defend an inflation target at 2% and the yen’s nominal anchor. Yet being truly irresponsible implies that the market starts to question whether the BoJ is willing or able to defend the inflation target from above. PPP valuations then become less relevant and domestic investors start permanently abandoning the currency. Things then get really volatile.

At the end of the day, the last two years' broad yen underperformance can only reverse when one simple thing happens: the Bank of Japan starts hiking rates, and far more than a tiny move to zero. When and if that happens, rather than FX intervention, is pretty much the only thing that matters.

По мнению DB на балансе Правительства Японии самый большой кэрри-трейд в мире объемом 20 трлн долл. и невозможно рассматривать нормализацию ДКП в Японии, не принимая во внимание последствия неизбежного сворачивания этого кэрри-трейда. И чем больше Банк Японии медлит - тем выше риски для финансовой стабильности и иены. Если Банк Японии будет действовать решительно, то цену за сворачивание кэрри-трейда заплатят богатые и пожилые, если промедлит - то цена ляжет на плечи молодых и мало-обеспеченных.

Далее в треде оригинальный текст на английском от DB, который разъясняет детали того, как устроен этот Кэрри-трейд.

The government of Japan is engaged in a massive $20 trillion carry trade. We argue that it is impossible to understand the consequences of Japanese monetary policy normalization without analyzing what it means for this carry trade. If the Bank of Japan decides to tighten policy meaningfully, this trade will need to unwind. If the Bank of Japan drags its feet to keep the carry trade going, it will require higher and higher levels of financial repression but ultimately pose serious financial stability risks, including potentially a collapse in the yen. Either option will have huge welfare and distributional consequences for the Japanese population: if the carry trade unwinds, wealthier and older households will pay the price of higher inflation via rising real rates; if the BoJ delays, younger and poorer households will pay the price via a decline in future real incomes. Which way this political economy question gets resolved will be key to understanding the policy outlook in Japan in coming years. Not only will it determine the direction of JPY but also Japan’s new inflation equilibrium. Ultimately, however, someone will have to pay the cost of inflation "success".

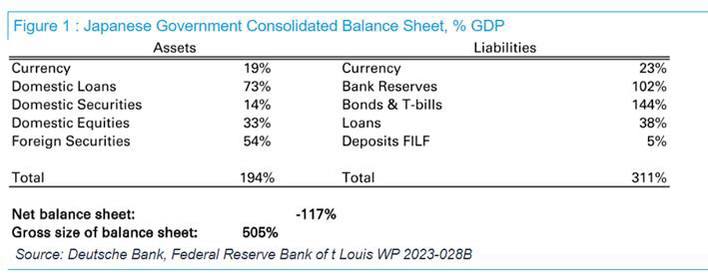

Our starting point is two excellent papers from the San Francisco Fed and IMF, which consolidate the Japanese government’s balance sheet to include the central bank (BoJ), state-owned banks (namely, PostBank) and pension funds (namely, GPIF)1. A consolidation of debt is absolutely crucial to understanding why Japan has not faced a debt crisis in recent decades given a public debt/GDP ratio of above 200% that continues to rise. It is also crucial to understanding what the impact of Bank of Japan tightening on the economy will be.

So what does the government’s consolidated balance sheet look like? We show below the results from the SF Fed paper. On the liability side, the Japanese government is primarily funded in low yielding Japanese Government Bonds (JGBs) and even lower-cost bank reserves. Over the last ten years the BoJ has effectively swapped out half of the entire JGB stock with even cheaper cash which it created, now held by banks. On the asset side, the Japanese government mostly owns loans, for example via the Fiscal and Investment Loan Fund (FILF), and foreign assets, primarily via Japan’s largest pension fund (the GPIF). The Japanese government's net debt position of 120% of GDP when accounting for all of this is one reason why debt dynamics have not been as poor as what would seem at first sight.

The first question that then arises is why hasn’t this carry trade blown up over the last few years given the huge sell-off in global fixed income? Everyone else has stopped out of carry trades, why hasn’t Japan? The answer is simple: on the liability side the BoJ controls the government's cost of funding and this has been kept at zero (or indeed negative) despite rising inflation. On the asset side, the Japanese government has benefitted from a massive depreciation in the yen which has raised the value of its foreign assets. Nowhere is this more evident than the GPIF, which has delivered cumulative returns in the last few years larger than the past two decades combined. The Japanese government has earned returns from both the FX and fixed income legs of the carry trade. It is not only the Japanese government that has benefitted, however. Falling real rates benefit every asset owner in Japan, predominantly older wealthy households. It is often claimed that an ageing population does well from low inflation. In fact, in Japan it is quite the opposite: older households have proven bigger beneficiaries of rising inflation via the de facto decrease in real rates and increase in value of the assets they own.

What will force this carry trade to unwind ? The simple answer is sustained inflation. Consider what would happen if inflation required the Bank of Japan to hike rates: the liability side of the government balance sheet will take a huge hit via higher interest payments on bank reserves and a decline in the value of JGBs. The asset side will suffer via a rise in real rates and an appreciation of the yen that causes losses on net foreign assets and potentially domestic assets too. The wealthy, older households will take a similar hit too: their asset values will drop while the fiscal capacity of the government to fund pension entitlements will erode. On the flipside, the younger households will be better off. Not only would they earn more on their deposits, the real rate of return on their future stream of savings would rise too.

Are there ways for the government to prevent the pain and required fiscal consolidation that higher inflation would create, especially on older households? Three options stand out.

Tax younger households.

Rather than reducing pension outlays to help improve the fiscal balance another alternative is to increase taxation too. The key constraint here would be a political one because older households are wealthier and have already been the primary beneficiaries of the Bank of Japan's QQE policy.

Prevent real rates from rising. In practice, this would mean that the Bank of Japan tolerates persistently higher inflation by staying behind the curve and eroding the real value of government debt. This is ultimately a variation of fiscal dominance which at its extreme would pose serious financial stability risks. If domestic households reach the conclusion that the yen’s monetary anchor is lost, we would ultimately see capital flight and a dramatic depreciation in the yen.

Don’t pay the banks. The single biggest funder of the Japanese government’s carry trade is the banking system via its large holdings of excess reserves. There is then one straightforward way of preventing the central bank (and by extension) the government’s interest bill from rising: apply reverse tiering to excess reserve balances by not paying interest. This is an approach that is already followed by Switzerland and may well work in the short-term. Ultimately, however, it creates serious financial stability risks because it prevents banks from passing on the full benefit of interest rate increases to depositors. The end result would be to create conditions for deposit flight similar to what we saw in the US regional banks crisis this year.

None of the options discussed above are sustainable over the long-term. However, they help highlight a menu of complementary policy choices that can be deployed to delay or attenuate the distributional trade-offs that a higher inflation regime in Japan creates.

The last few years of extremely easy monetary policy have been relatively straightforward from a Japanese political economy perspective: falling real rates, improving fiscal space and income redistribution that has favoured wealthy, older voters. If Japan is indeed embarking on a new chapter of structurally higher inflation, however, the choices going forward are likely far less easy. Adjusting to a higher inflation equilibrium will require rising real rates and greater fiscal consolidation, in turn more damaging to older and wealthier voters, unless the younger voters get taxed. This adjustment can be delayed but at the cost of rising financial stability risk and a weaker yen. The yen, in turn, can only embark on a sustained uptrend when the Japanese government – via BoJ rate hikes – is forced to unwind the world's last big surviving carry trade in the post-COVID world.

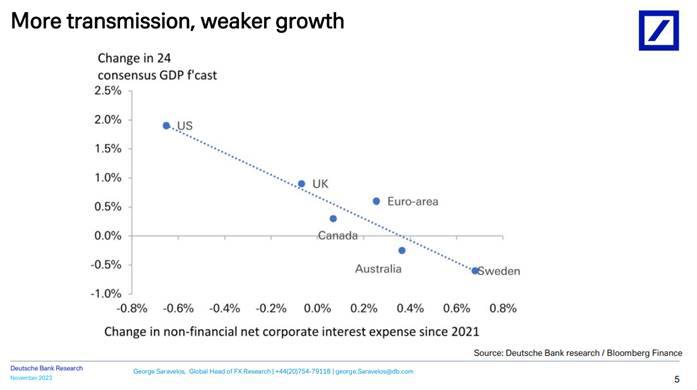

📌 The dollar has stayed strong this year on a very big widening in US – global growth differentials and high real rates. This is mostly because tight Fed policy is not yet transmitting to the US economy like elsewhere and Americans are spending their excess savings while others aren’t.

📌 For the dollar to turn the Fed needs to pivot dovish and cut more than other G10 central banks. However, the risks versus market pricing are that the Fed easing cycle is delayed and the dollar remains a high-yielder. There is also now very little safe-haven risk premium priced in to the USD despite high (geo)political risks next year.

📌 European currency fundamentals are strong, this is reflected in a very high trade-weighted exchange rate. The turn in EUR/USD is therefore more a function of the broader dollar. We see EUR/USD range-bound below 1.10 for most of next year unless and until the Fed pivots dovish. There are risks the ECB cuts first, pushing EUR/USD closer to parity, with German fiscal policy following the Constitutional Court decision a notable downside risk.

📌 The Japanese government is running a huge carry trade, funded in short-dated bank liabilities and invested in long duration domestic and foreign assets. This could slow down the Bank of Japan and create fiscal dominance risks. JPY will only strengthen when the BoJ starts a proper hiking cycle or the Fed cuts rates.

📌 The Chinese balance of payments is suffering from structural decoupling. Combined with a need for lower real rates to help the Chinese economy deleverage this means the CNY should continue to underperform.

📌 EM FX performance does not depend on a Fed easing cycle but the global growth backdrop. The most bullish outcome for EM FX is a positive global supply shock, ie Fed easing in a soft landing. Falling equities and falling yields (ie, a recession) are the worst outcome. US growth outperforming with inflation coming down should be best for EM carry.

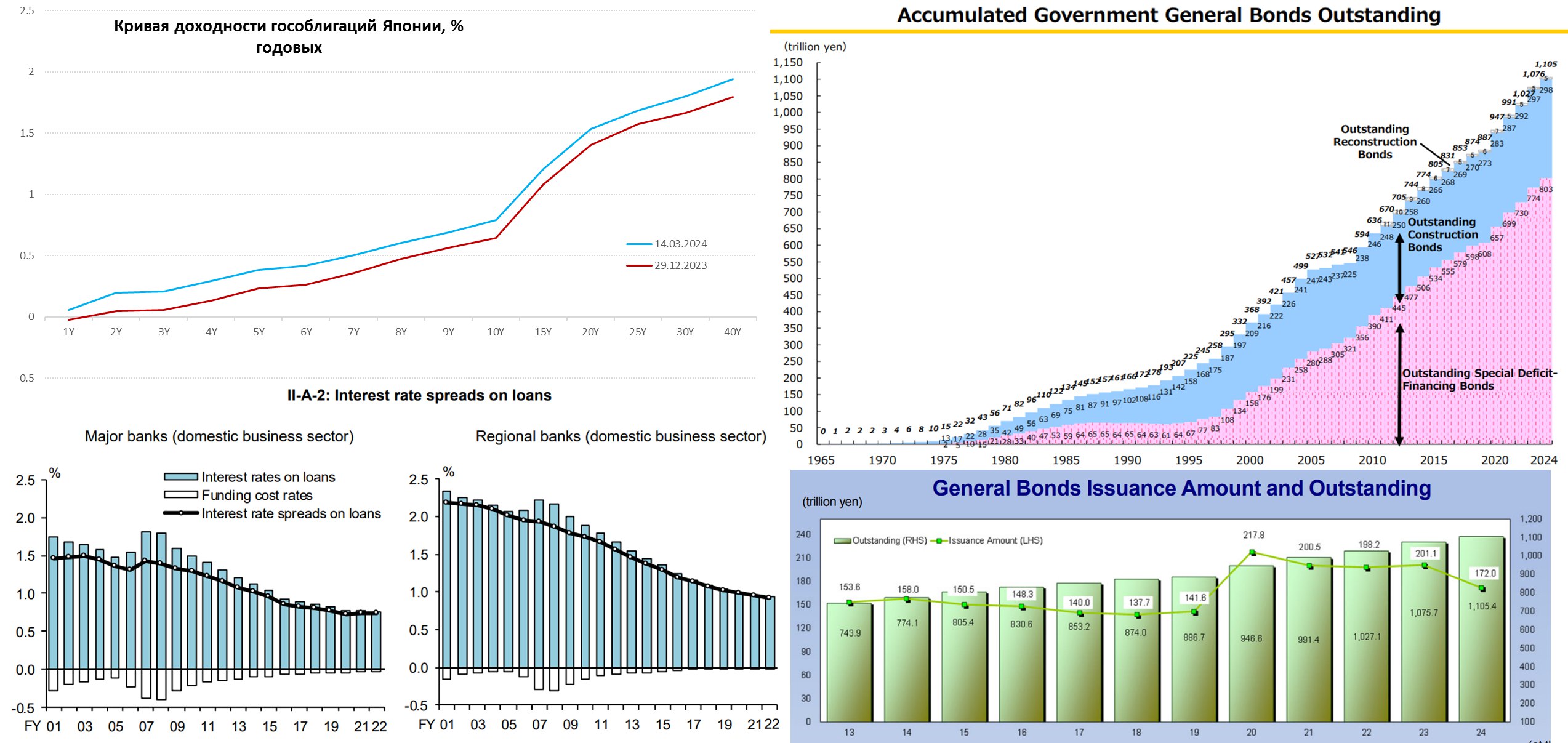

На рынках с некоторым азартом обсуждают тему завершения эпохи отрицательных ставок в Японии, особенно после новостей о том, что профсоюзы договорились о рекордной для страны за три десятилетия индексации зарплат в среднем на 5.3%. При этом, экономика Японии в состоянии около рецессии, но и шансы досидеть до разворота ФРС существенно понизились после отчетов по инфляции в США. Хотя рынки активно спекулируют на тему разворота – в реальности пока не очень ставят на активные действия Банка Японии, о чем говорит как курc йены у 150, так и доходность десятилеток у 0.8%.

Огромный навес внутреннего долга в 400% ВВП, из которых более половины – госдолг, выпущенный по околонулевым ставкам вряд ли оставляет Банку Японии большое пространство для маневра. Процентный спред японских банков чуть выше 0.5%, любые резкие движения создадут для них проблемы. Не говоря уже о правительстве, которое с долгом более 200% ВВП и облигациями на ¥1.1 квдрлн ($7.4 трлн), пусть даже ¥0.6 квдрлн ($4 трлн) выкупил ЦБ, вряд ли может себе позволить значимый рост ставок.

Учитывая, что Минфин Японии запланировал рост процентов по долгу с ¥8.5 трлн до ¥9.7 трлн, а координация между Минфином и ЦБ очень высокая. А также то, что рефинансироваться должно 15-16% госдолга, Минфин Японии закладывает рост ставки в пределах 0.5 п.п. в 2024 финансовом году (до апреля 2025), т.е. сама ставка в реальном выражении останется глубоко в отрицательной области (инфляция 2-3%), но большего они себе позволить не могут. Уйти от интервенций в госдолге Банк Японии вряд ли сможет – он будет держать рынок, иначе спекулянты его быстро сломают и порезвятся.

Какие процессы это может запустить вопрос открытый, керри-трейд все-равно сохранится, хотя огромный навес спекулятивных позиций может заиграть новыми красками. Портфельные инвестиции Японии во внешний мир составляют $4.5 трлн из которых $2.1 трлн – акции и фонды, $2.4 трлн – облигации. По данным Минфина США только напрямую японцы являются крупнейшим неофшорным держателем американских ценных бумаг на $2.5 трлн (больше только у Лондона, который держит бумаг США на $2.8 трлн). Портфель Японии в США: акции $0.9 трлн, облигации $1.6 трлн, из них $1.05 трлн – гособлигации США. Плюс у Японии еще деривативов на внешних рынках $0.5 трлн в обе стороны.

Если японские капиталы задвигаются – то это может поднять определенные волны на рынках, но стоит помнить, что власти Японии очень плотно координируют свои действия с Минфином США, в апреле как раз у Йеллен профицитный бюджет. Деваться Банку Японии в любом случае некуда ... досидеть пока ФРС развернет надежд мало, последние пару лет падение реальных доходов выливается в индексацию з/п, при сохранении инфляции. Но действия пока скорее будут скорее символическими, т.е. вряд ли что изменят по сути, хотя могут провоцировать новые спекулятивные игры.

@truecon

К вербальным интервенциям против ослабления йены подтянулся и премьер Японии Кисида.

Самое забавное, что в это же время он завил, что Банку Японии целесообразно сохранять мягкие денежно-кредитные условия, Правительство сохранит тесное взаимодействие с ЦБ и пообещал опережающий относительно инфляции рост зарплат. В общем за все хорошее и против всего плохого ... но падение йены фундаментально необоснованно.

Каждый подход к 152 йен за доллар провоцирует бурный поток слов, но пока не действий. Учитывая, что подтянулся уже и премьер, на которого курс не отреагировал, скоро рынок вытащит ЦБ на интервенции.

@truecon

ПП

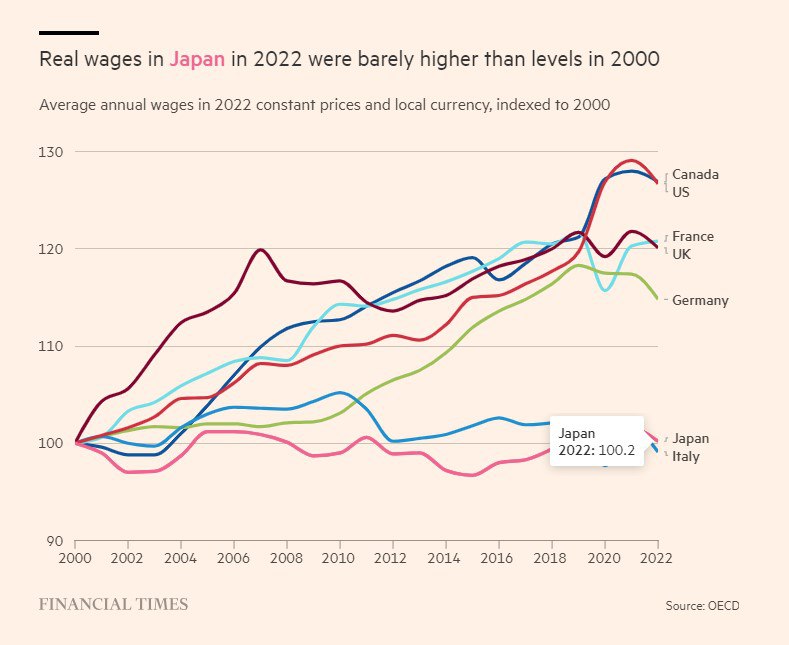

С 1990-х годов Япония была единственной развитой экономикой в мире, где инфляция, процентные ставки и рост зарплаты оставались близкими к нулю, а в некоторых случаях и ниже него. Однако с весны 2022 года на фоне двух шоков (пандемии Covid-19 и конфликта Россия - Украина) цены в Японии начали расти. Базовая инфляция, которая исключает волатильные цены на продукты питания, выросла в феврале на 2,8% г/г.

Крупнейшие работодатели страны согласились повысить заработную плату в среднем на 5,3% весной 2022 года, что стало самым большим увеличением с 1991 года.

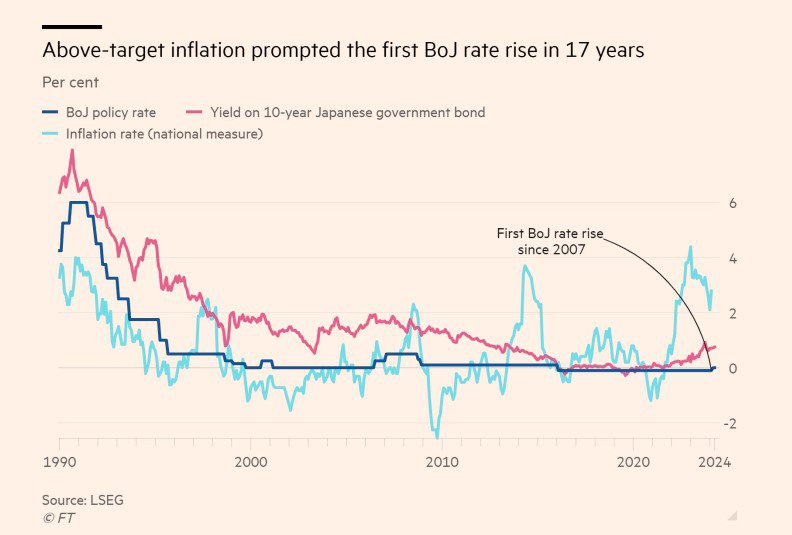

В феврале этого года фондовый индекс Nikkei 225 наконец превзошел предыдущий пик, достигнутый 34 года назад. В следующем месяце Банк Японии завершил цикл отрицательных ставок, один из самых противоречивых экспериментов в области ДКП, повысив стоимость заимствований впервые с 2007 года.

Глава Банка Японии заявил в марте, что центральный банк сможет проводить «нормальную ДКП» после прекращения контроля над кривой доходности.

Тем не менее, некоторые экономисты указывают на медленное принятие обществом идеи постоянного роста цен, в то время как другие спорят, насколько точно официальные экономические данные отражают реальную картину мира. Вместо этого многие призывают ЦБ действовать медленно и отвергать необходимость устойчивых повышений ставок, как это делают в Европе и США.

За этой осторожностью стоят структурные проблемы – сокращение и старение населения, высокий госдолг, по сравнению с размером экономики – и возникновение дефляции в других местах. Китай, в частности, сейчас борется с падением цен, и замедление темпов роста будет иметь серьезные последствия для мировой экономики.

Несмотря на то, что инфляция потребительских цен уже почти два года превышает целевой показатель Банка Японии в 2%, объявлять об окончании дефляции преждевременно. Потребление остается слабым, а курс иены упал до самого низкого уровня за 34 года, поскольку инвесторы ожидают, что процентные ставки в Японии будут близкими к нулю, даже если ставки в США и других странах останутся повышенными.

Одним из основных источников неопределенности остается вопрос, распространится ли резкое повышение заработной платы крупнейшими компаниями Японии на малые и средние предприятия, где заняты 70% населения. Повышение зарплат может ударить по бизнесу. Японские компании склонны поглощать инфляцию, а не трансформировать ее в рост цен. В 2023 году количество банкротств предприятий выросло на треть, и большая часть пришлась на секторы, где был наиболее высокий рост стоимости рабочей силы (строительство и сфера услуг).

Экономисты отмечают, что решение центробанка считать экономику Японии нормализованной преждевременно и не основывается на реальности стагнирующего делового цикла. Обещание Банка Японии продолжать покупать около 6 трлн йен 10-летних японских гособлигаций ежемесячно является еще одним признаком того, что до нормальной ДКП еще далеко.

В то же время японские акции вступили в необычайно продолжительный бычий рынок. Инфляция толкает местных инвесторов искать способы получить доходность в изменившихся условиях. А глобальные игроки переоценивают стоимость японских компаний по меркам остального мира.

Руководители компаний отмечают, что на протяжении 5-10 лет потребуются повторные повышения заработной платы в среднем на 3%, в то время как инфляция должна находиться на уровне в 2%. Тогда ситуация в экономике начнет нормализовываться.

🇯🇵Тред про экономику Японии можно прочитать тут.

@emcr_experts

Банк Японии, пожалуй, выдал самый короткий стейтмент после заседания по ставке из 7 строчек.

decided, by a unanimous vote, to set the following guideline for money market operations for the

intermeeting period:

The Bank will encourage the uncollateralized overnight call rate to remain at around 0 to

0.1 percent.

Regarding purchases of Japanese government bonds, CP, and corporate bonds, the Bank will

conduct the purchases in accordance with the decisions made at the March 2024 MPM."

Ставка остается прежней, все остальное как сказано в марте... точка. В общем-то это лучше всего говорит о том, в каком состоянии находится ЦБ. В квартальном обзоре Банк Японии немного ужесточил сигнал по инфляции, заявив о том, что ожидает инфляцию у целевого уровня ... потом в 2025/26 годах.

Рынок, конечно, продолжил проваливать и йену, видя беспомощность ЦБ. На что Минфин Японии ответил очередным последним японским предупреждением... но это мало на что влияет, пока не будет активных действий - будут давить.

Скорее всего, конечно, власти готовят интервенцию, чтобы "шокировать" рынки, но пока ситуация со ставками не изменится, все эти интервенции будут иметь лишь временный эффект.

@truecon

Иена сегодня снова обвалилась до новых исторических минимумов после заседания Банка Японии. Мы считаем, что это оправдано, и что день, когда рынок понял, что Япония следует политике благосклонного пренебрежения к иене, наконец настал. И угроза интервенций не является убедительной.

The yen has again collapsed today to fresh record lows following the Bank of Japan meeting. We think this is warranted and that this finally marks the day where the market realizes that Japan is following a policy of benign neglect for the yen. We have long argued that FX intervention is not credible and the toning down of verbal jawboning from the finance minister overnight is on balance a positive from a credibility perspective. The possibility of intervention can't be ruled out if the market turns disorderly, but it is also notable that Governor Ueda played down the importance of the yen in his press conference today as well as signalling no urgency to hike rates. We would frame the ongoing yen collapse around the following points.

1. Yen weakness is not that bad for Japan. The tourism sector is booming, profit margins on the Nikkei are soaring and exporter competitiveness is increasing. True, the cost of imported items is going up. But growth is fine, the government is helping offset some of the cost via subsidies and core inflation is not accelerating. Most importantly, the Japanese are huge foreign asset owners via Japan's positive net international investment position. Yen weakness therefore leads to huge capital gains on foreign bonds and equities, most easily summarized in the observation that the government pension fund (GPIF) has roughly made more profits over the last two years than the last twenty years combined.

2. There simply isn't an inflation problem. Japan's core CPI is around 2% and has been decelerating in recent months. The Tokyo CPI overnight was 1.7% excluding one-off effects. To be sure, inflation may well accelerate again helped by FX weakness and high wage growth. But the starting point of inflation is entirely different to the post-COVID hiking cycles of the Fed and ECB. By extension, the inflation pain is far less and the urgency to hike far less too. No where is this more obvious than the fact that Japanese consumer confidence are close to their cycle highs.

3. Negative real rates are great. There is a huge attraction to running negative real rates for the consolidated government balance sheet. As we demonstrated last year, it creates fiscal space via a $20 trillion carry trade while also generating asset gains for Japan's wealthy voting base. This encourages the persistent domestic capital outflows we have been highlighting as a key driver of yen weakness over the last year and that have pushed Japan's broad basic balance to being one of the weakest in the world. It is not speculators that are weakening the yen but the Japanese themselves.

The bottom line is that for the JPY to turn stronger the Japanese need to unwind their carry trade. But for this to make sense the Bank of Japan needs to engineer an expedited hiking cycle similar to the post-COVID experiences of other central banks. Time will tell if the BoJ is moving too slow and generating a policy mistake. A shift in BoJ inflation forecasts to well above 2% over their forecast horizon would be the clearest signal of a shift in reaction function. But this isn't happening now. The Japanese are enjoying the ride.

How do I join the thread?

EMCR NEWS: INSTRUCTIONS

How to Join EMCR News Discussions

The EMCR News - feed is akin to the Bloomberg news line. In it, you will find the latest financial news, along with associated comments and discussions from professional analysts.

To not miss anything - read the full EMCR News feed on the EMCR website through a desktop or a pinned browser window on the "home" screen of your phone.

How to pin the EMCR News window: Instructions for iPhone, instructions for Android

How to join the EMCR News feed as a contributor and participant?

Step 1: Create and adequately complete your personal or corporate profile on the EMCR professional social network.

Step 2: Get verification of your expertise from someone who already has a verified personal profile on EMCR.

Step 3: in the settings of your personal or corporate profile, connect the broadcast of your Telegram channel to the profile.

After this, the content of your channel will be displayed in your EMCR profile. We can include the most interesting of your posts or all of your content in the EMCR News feed depending on its quality and topic. You will also be able to participate in news discussions and link your posts in long thematic threads.

Participating in EMCR News discussions and linking your posts to threads.

To comment on some news, copy the link to it from the source Telegram channel and paste it in your comment or make a repost of the news from the source channel in your own channel and give your comment as a reply to this repost If your comment enters the news discussion on EMCR News, it will look like this: EXAMPLE

You can also comment on other participants comments (also through a link or repost) and they will also be added to the general chain of comments.

ATTENTION: only professional comments get into the news discussion.

A thematic thread is a series of comments about one topic, connected to each other.

EXAMPLE

Linking your posts to thematic threads is also done through a reply to your previous post or by inserting the link to it as the first link in your new post.

We share the best threads and discussions in our "Thread of the Day" section, and also share them in our @EMCR_jobs channel.

We wish you interesting posts and great discussions!